Managing finances can often feel overwhelming, especially for young professionals and millennials balancing new responsibilities and lifestyle desires. If you’ve been wondering where your money vanishes every month despite earning a decent paycheck, you’re not alone.

That’s where the 50/30/20 budgeting rule comes in—a simple and effective framework to regain control of your finances while ensuring a balance between enjoying life and saving for the future. This blog dives deep into the 50/30/20 rule, its relevance for the Indian context, and actionable steps for implementing it to achieve financial stability.

Table of Contents

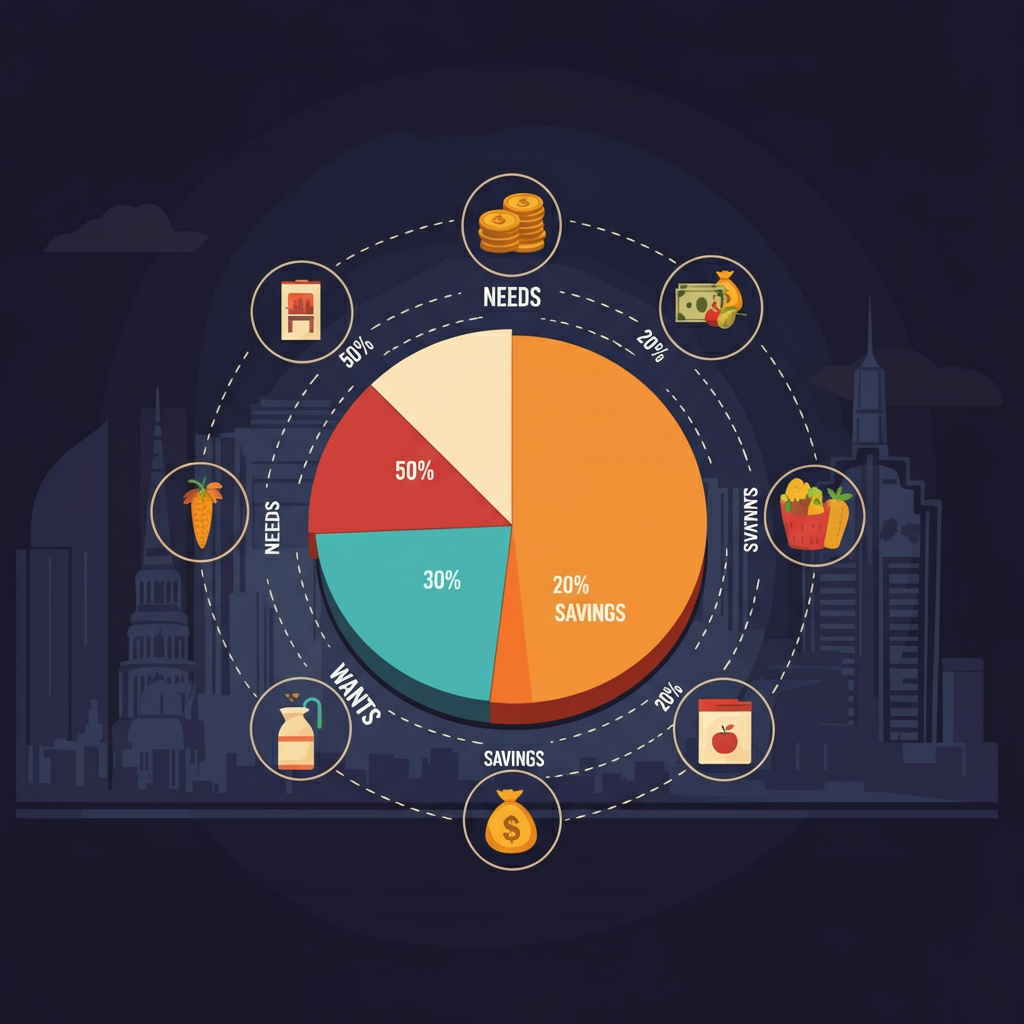

Understanding the 50/30/20 Rule

The 50/30/20 rule is a straightforward budgeting strategy to allocate your after-tax income into three broad categories:

- 50% for Needs: Essential expenses that are non-negotiable.

- 30% for Wants: Discretionary spending that enhances your lifestyle.

- 20% for Savings and Investments: Building financial security for the future.

By following this rule, you get a blueprint to avoid overspending, prioritize savings, and mindfully manage your wants.

What Falls Under Each Category?

1. Needs (50%)

Needs refer to the essentials required for survival and maintaining a basic standard of living.

Examples of needs include:

- Rent or home loan EMI

- Utilities (electricity, water, internet)

- Groceries and daily essentials

- Transportation costs (fuel, public transport)

- Insurance premiums (health, car)

- Minimum debt repayments

The goal here is to keep these expenses within 50% of your income. If needs exceed this, it’s crucial to reassess your spending or compromise on wants temporarily.

2. Wants (30%)

Wants are non-essential expenses that contribute to enjoyment and fulfillment but aren’t critical for day-to-day living.

Examples of wants include:

- Dining out or ordering food

- Netflix and OTT subscriptions

- Hobbies and leisure activities

- Shopping for non-essentials (fashion, gadgets)

- Vacation and travel

Wants often blur with needs, making it essential to draw a clear line. For example, groceries are a need, but expensive chocolate or premium coffee brands are wants.

3. Savings and Investments (20%)

This category focuses on building your financial safety net and creating long-term wealth.

Examples of savings and investments include:

- Emergency funds

- Fixed deposits or recurring deposits

- SIPs and mutual funds

- Stock market or PPF investments

- Retirement funds (NPS, EPF)

Automating your savings through recurring transfers ensures discipline and eliminates the temptation to overspend from this category.

Read More: How to Start Investing in Stocks in India: A Beginner’s Complete Guide,

How to make a monthly budget in 5 simple steps

Applying the 50/30/20 Rule in India

Here’s how Indian professionals can implement this budgeting framework in real-life scenarios based on varying income levels and circumstances.

Scenario 1: The Recent Graduate

A fresh graduate earning ₹30,000 monthly can structure their budget as:

- Needs (₹15,000): Rent (₹10,000), utilities (₹2,000), groceries (₹3,000).

- Wants (₹9,000): Dining out, clothes shopping, movies.

- Savings (₹6,000): Building an emergency fund or starting mutual fund SIPs.

Scenario 2: The Young Family

A young family with a combined income of ₹80,000 could plan like this:

- Needs (₹40,000): Housing, groceries, childcare, and bills.

- Wants (₹24,000): Family outings, entertainment, hobbies.

- Savings (₹16,000): Education funds, retirement investments.

Scenario 3: The Freelancer

For freelancers with fluctuating income (averaging ₹50,000 per month), flexibility is key:

- Needs (₹25,000): Shared housing, utilities, groceries.

- Wants (₹15,000): Professional courses, leisure expenses.

- Savings (₹10,000): Emergency fund and irregular income buffer.

Challenges and How to Overcome Them

While the 50/30/20 rule is simple, real-world implementation can bring certain challenges.

1. Income Fluctuations

Solution: Base percentages on a conservative average income (e.g., your lowest monthly income). Include an irregular income buffer within savings.

2. High Cost of Living

Solution: If you live in cities like Mumbai or Delhi, cut back on spending for things you want. You can also look for ways to earn more money, like freelancing or side jobs.

3. Debt Repayment

Solution: Allocate part of the “needs” budget to aggressive debt repayment. Consider balancing this by reducing wants temporarily.

4. Lifestyle Creep

Solution: With rising income, keep the basic 50/30/20 proportions intact and direct raises toward savings rather than wants.

5. Lack of Tracking

Solution: Use budgeting apps like Walnut or Mint to monitor your spending and identify areas for improvement.

Tools and Resources

Budgeting becomes a breeze with the right tools and resources. Here’s what can help you stay on track:

- Budgeting Apps: Options like Mint, Wallet, and Splitwise can automate expense tracking.

- Spreadsheets: Create a personalized budget spreadsheet that categorizes your expenses into needs, wants, and savings.

- Reading Material: Books like Rich Dad Poor Dad and The Psychology of Money offer actionable financial insights.

- Automated Savings: Set up recurring deposits for savings or investments directly from your salary account.

- Online Forums: Join communities like Reddit’s r/PersonalFinanceIndia to engage with like-minded individuals.

Adjusting the Rule for Individual Preferences

The 50/30/20 rule is not a rigid framework—it can be customized to fit unique financial situations.

- High Debt: Allocate more than 20% to savings by reducing wants until debts are under control.

- Single Income Household: Reduce wants to 20% or lower to ensure adequate savings.

- High Income: Maximize savings by lowering wants to build wealth faster.

Regularly review your budget to adapt to changing circumstances, such as pay hikes, job changes, or shifting family priorities.

Why Following the 50/30/20 Rule is Worth It

Adopting the 50/30/20 rule brings numerous benefits:

- Promotes financial discipline by setting clear spending boundaries.

- Builds an emergency fund and investment portfolio for long-term stability.

- Reduces the stress of paycheck-to-paycheck living.

- Encourages mindful spending habits aligned with personal goals.

By dividing and conquering your finances, you simplify money management and gain the confidence to secure your financial future.

Start Budgeting Today for a Secure Tomorrow

The 50/30/20 budgeting rule offers an accessible and adaptable approach to take control of your money. Whether you’re a recent graduate, young family, or seasoned professional, this rule can be your guide to achieving financial balance and freedom.

Start today! Review your after-tax income, categorize expenses into needs, wants, and savings, and take the first step toward financial empowerment.

Your financial peace of mind is just one budget plan away.

Related Post:

10 Best Money Management Apps in India for Better Financial Control

2 thoughts on “What is the 50/30/20 rule for budgeting?”